Learn

Dollar-Cost Averaging Explained (DCA): The Easiest Way to Start Investing

September 24, 2025

9 min read

Discover compound interest explained with real tables—€50, €100, €500, and €1000 per month—plus formulas, calculators, and practical tips.

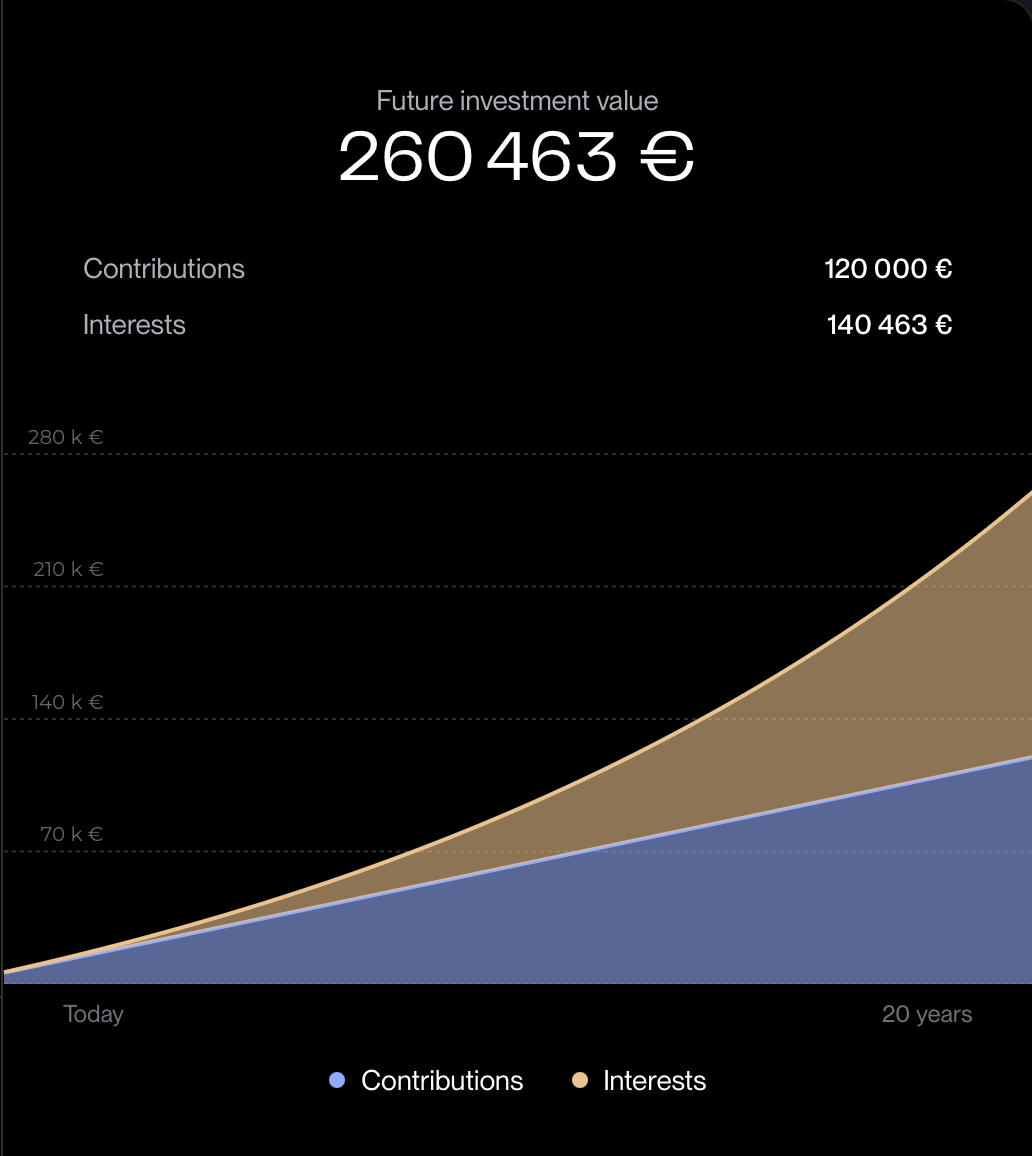

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” When you see compound interest explained in action with a compound interest calculator, it becomes clear why: small sums can snowball into surprisingly large totals.

In this guide, we’ll walk through compound interest examples with real numbers—€50, €100, €500, and €1000 per month—so you can see how your money might grow over time.

Compound interest is interest earned on both your original money and on the interest that has already been credited. This “interest-on-interest” effect is what accelerates growth, even with small, regular contributions (SEC, Investor.gov 2025). Put simply: invest regularly, earn returns, then let those returns earn more.

The compound interest formula for a lump sum is:

A = P × (1 + r/n)^(n×t)

For monthly investment compound interest, calculators use the future value of a series formula:

FV = PMT × [((1 + i)^N − 1) / i]

Where PMT = monthly payment, i = r/12, and N = 12×t (SEC, Investor.gov Compound Interest Calculator 2025).

Assumptions: monthly contributions at month-end, annual rates of 4% and 7%, monthly compounding, no fees or taxes. Actual results vary; fees and taxes reduce returns (SEC, Mutual Fund and ETF Fees Bulletin 2025; HMRC, Savings Tax Guide 2025).

A compound interest calculator lets you adjust timeframes, monthly inputs, and rates. Beginners can see how small contributions add up and understand the trade-off between starting now versus later (FINRA, 5 Steps to Take Control of Your Finances 2024).

Because planning with actual budgets shows how achievable compounding is. Even modest amounts illustrate how growth accelerates the longer you stay invested (CFPB, ConsumerFinance.gov 2023).

Changing from 4% to 7% nearly doubles 30-year outcomes in our tables. But higher expected returns come with higher risks, so always test a range (SEC, Investor.gov 2025).

Now you understand well how compound interest work, you should try a real time simulator like this one: Compound Interest Calculator.

The earlier you start, the more “cycles” of compounding you benefit from. Ten extra years can outweigh bigger deposits made later (CFPB).

Because your returns also generate returns. Early investing multiplies growth more effectively than waiting to invest larger amounts (SEC).

Compound interest rewards time, patience, and consistency. Whether you invest €50 or €1000 per month, the real growth comes from letting your money work on itself. Use a compound interest calculator, choose realistic rates, and give compounding time to do its work (SEC).

Try 4%–7% for a balanced view; higher rates mean more growth but also more risk (FINRA).

Monthly is common in calculators; more frequent compounding gives a slight boost but contributions matter more (SEC).

Yes, debts can compound too—making them grow faster if unpaid (CFPB).

Yes, both reduce returns significantly; always check account charges and tax rules (HMRC; SEC).

Historically possible but never guaranteed; test conservative and moderate rates (SEC; FINRA).

SEC, Investor.gov Compound Interest 2025 ; SEC, Compound Interest Calculator 2025 ; SEC, Mutual Fund and ETF Fees Bulletin Jul 23, 2025 ; SEC, Saving and Investing Guide PDF Feb 2019 ; CFPB, How Does Compound Interest Work? Nov 7, 2023 ; FINRA, 5 Steps to Take Control of Your Finances Jan 9, 2024 ; FINRA, Financial Education PDF Jun 2025 ; HMRC, Savings Tax Guide Mar 3, 2025 ; HMRC, Personal Savings Allowance Dec 9, 2015.

Fintech analyst and Web3 enthusiast. I break down the economic models of protocols, compare yields (staking, restaking, RWA), and simplifies risk analysis for retail investors.